Annuities are products filled with possibilities. The only problem is how few people know about them. That’s why Annuity Awareness […]

Annuities are products filled with possibilities. The only problem is how few people know about them. That’s why Annuity Awareness […]

Asian American and Pacific Islander (AAPI) entrepreneurs have been making bold moves in the financial services industry today. Despite barriers […]

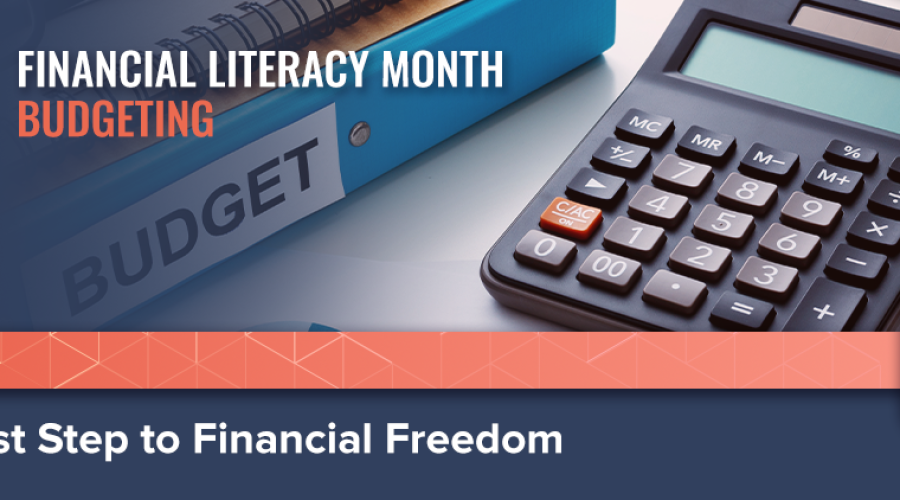

April is Financial Literacy Month, a time to focus on building strong financial habits that set you up for long-term […]

April is Financial Literacy Month, a time to focus on building strong financial habits that set you up for long-term […]

April is Financial Literacy Month, a time to focus on building strong financial habits that set you ovup for long-term […]

April is Financial Literacy Month, a time to focus on building strong financial habits that set you up for long-term […]

April is Financial Literacy Month, a time to focus on building strong financial habits that set you up for long-term […]

As a financial entrepreneur, you have plenty of different ways to market your business — but without the big budgets […]

In the financial services industry, trust is everything. People want to work with someone who is knowledgeable, confident and genuinely […]

The need for financial services is evolving faster than ever; if you are an entrepreneur, 2025 presents unique opportunities for […]

October is Financial Planning Month, and while learning to manage your own finances first is important, it’s also the perfect […]

October is Financial Planning Month, a perfect time to focus on taking control of your financial future. Whether you’re starting […]

© 2025 · First Financial Security, Inc. All Rights Reserved. | Site Map | Privacy Statement